There’s no doubt that there will be a big impact of Brexit throughout the EU’s economy with the UK being predicated by many as the biggest loser. But who will be the biggest winner? In this piece of analysis I will outline why I believe Dublin city centre and particularly the IFSC micro-economy will benefit, and how this will impact on the property market in this area.

Global companies choose Dublin for access to European Financial Markets

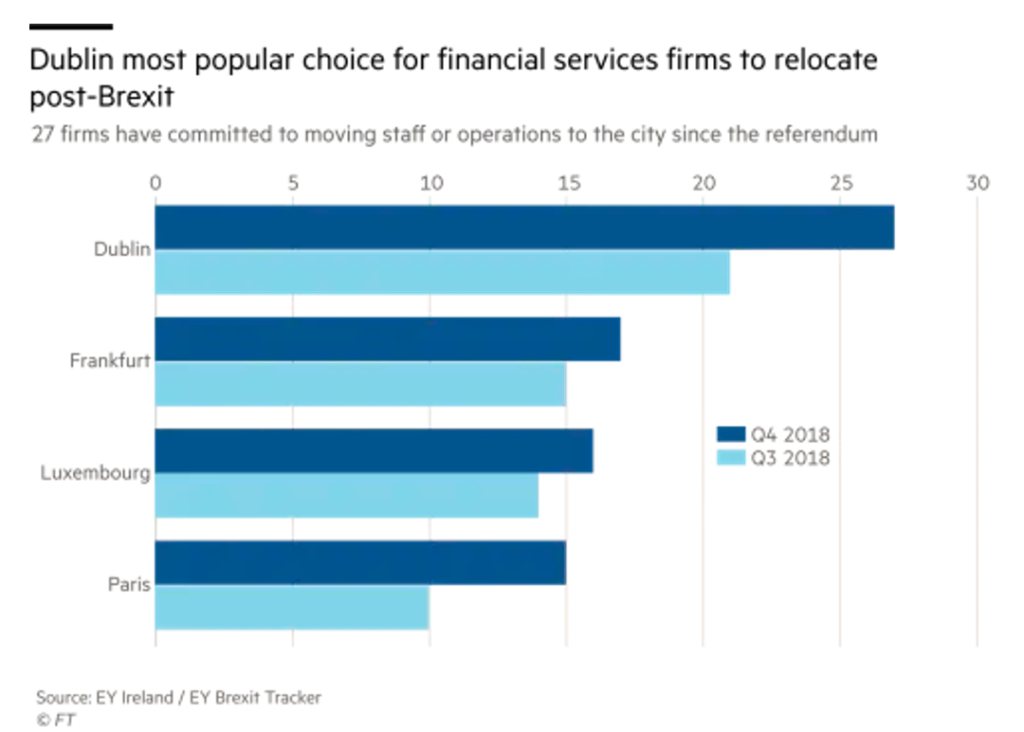

According to EY, Dublin is the preferred location in Europe for both global companies looking to grow by access the European markets, and also by UK companies looking to maintain access to this market. But why Dublin?

Post-Brexit, Ireland will be the only country in the EU which will have English as its primary language which makes it a priority location for US, UK and Asian companies whose corporate language is English. Add into the mix the young, highly-educated multi-lingual workforce available in Dublin, its attractive corporate tax status, pro-business financial regulation and it’s easy to see why Dublin is a very compelling argument for international banks and insurance companies to have their EU HQ there.

By setting up in Dublin, financial services companies can passport their products and services throughout the EU without the need for governmental regulation in each separate country. So if an Asian or American fund wants to enter the European financial services, they would just set up a European HQ or “hub”, and then distribute throughout the other jurisdictions. Similarly the UK, which has pre-Brexit access to these markets, but after Brexit these rights will be removed, irrespective of Deal or No Deal.

This is why Dublin is the no.1 location for UK financial services companies looking to move more assets and staff to Dublin to maintain access to the important European markets.

It’s no secret that companies like Barclays, JP Morgan, Bank of America have invested heavily in Dublin for the long-term. They have moved billions of euro in capital, and have also entered long term office leases as they transfer their highly paid UK workers to Dublin and hire additional local staff. For example, in 2019 Barclays Bank moved €190bn worth of assets to Ireland, with UK-based workers to follow.

The IFSC isn’t a short term fad, but is a long term government backed strategy to provide simplified and stable access to European financial services markets. From humble beginnings back in the early 1990s, Dublin’s International Financial Service’s Centre (IFSC) has now over €5 trillion worth of asset under administration. The global bank Citibank have a presence in Dublin for over 50 years and which now employers over 9,000 at its European hub. Their competitors also have a large presence in Dublin including J.P. Morgan (c.1,000 employees), State Street (c. 2,500), BNY Mellon (c.1,700).

IFSC Fun Facts and Figures

500+ banks, insurers, finance and fund service companies

Over 1,000 different fund managers

Average salary of €60,100 (c. €3,500 net per month)

Total Direct Employment of over 38,000

Comprises 5% of all EU 27 cross-border financial services activity

All the global advisers: KPMG, EY, Grant Thornton, Deloitte, PwC

All the global legal firm: Dentons, Walkers, DLA Piper

Brexit Impact on Dublin Property Market

As more companies are attracted to Dublin because of Brexit, this will increase the demand for both local talent and the demand for local rental housing. This will mean that salaries will and rent will both rise.

The influx of overseas workers has exacerbated Dublin’s already chronic housing shortage and has led to very high demand for rental accommodation. As property prices are growing slower than the rate of the rents, the result is that Dublin has now the highest rental yields in any major European capital city.

The average cost of a 1 bed apartment in Dublin 1 (which includes IFSC) is €250,000 and generates an average rent of c. €1,605 resulting in a 7.7% yield. This monthly rent is still less than 50% of an average IFSC workers net income which is affordable considering the high quality, close proximity to their place of work and is often shared with a partner. With new insurers and banks companies coming to Dublin to access the European markets, this is leading to further increases in demand and upward pressure on rent, which is only compounded by the higher than average salaries in the IFSC. So whilst IFSC rents are higher than other parts of the Dublin, the average salaries are higher and increasing at a higher rate than the rents. The result is long queues for newly vacant apartments which I predict will last long after Brexit.

Contact me at colin@spirecapital.ie to see how Spire Capital can help you capitalise on IFSC property market.

Prices from: €495,000 Rental yields: 6% – 8%

Spencer Dock is an exciting development of 1, 2 and 3 bedroom apartments, penthouses and offices setting new standards in urban living and working. Designed by the famous Architects Scott Tallon Walker, it is hailed as the new city quarter

“Why is a multi-family home a better buy to let investment than a single-family home”

If you're looking to actively invest in residential property, most investors will consider two types: single-family home or multi-family home. With single-family, you'd be buying traditional homes built for one family or household. On the multi-family side, you’d be buying apartment buildings. Both are very attractive and popular but investors need to consider there are significant differences in terms of cashflow, risks, maintenance and returns on investment. We have explored some of these points below.

In single-family homes there is not a strong cash flow (unless you own several properties). Fewer units means less cash. You're only getting a handful of rent payments per month, and a large chunk of those are going toward your mortgage, maintenance costs, and admin fees. However in multi-family homes you have a better cash flow and a bigger financial cushion. The extra cash that comes with multi-family real estate can help safeguard you from loss. There's more room for error, and you may have more capital to further grow your investing business if you do it right.

“Buying a multi-family home means an instant real estate portfolio”

If you’re looking to build a big real estate portfolio single-family homes are not the way to go. A portfolio of 10 units would mean 10 negotiations, 10 mortgage applications, and 10 closings, and it would take much more time compared to multi-family properties which let you scale up with just one purchase. Buying a multi-family home means an instant real estate portfolio. You'll have at least several units on your hands, and having the cash flow and profits that come with it isn’t such a bad thing either!

“If a tenant moves out of a single-family rental, it is 100% vacant”

Yes single-family homes are a lot easier to acquire but when it comes to growth this would be slower than the multi-family homes. Also one of the disadvantages of a single-family homes is that if the property is vacant you would have zero income until the management company replaces the tenants whereas with a multi-family home they can lose a tenant but can still produce an income with the other occupied units. It is rare to see a multi-family home totally vacant. Multi-family rental owners are also far less likely to have zero rental income. If a tenant moves out of a single-family rental, it is 100% vacant. On the other hand, if a multi-family rental owner loses a tenant, its only 10% vacant. Even after that reduction in cash flow, you’ll still have 90% of your regular monthly rental income to cover the property’s mortgage and operating costs.

In single-family homes, if you want to make repairs or improvements to the building it only increases the value of that one property as opposed to many in a multi-family property. Financing the purchase of multi-family homes is much easier than of single-family investment properties. The return on investment received by investing in single-family rentals tends to be higher than from other rental types; however, banks are more easily persuaded to give a mortgage to real estate investors for multi-family properties due to the risks being lower.

When you base it on a per-unit basis, the cost of constructing a multifamily property is more affordable than other types of real estate properties. It is, therefore, a more cost-efficient investment and relatively risk-free for first-time investors. If you choose to apply for a mortgage loan to build or purchase this type of property, you can expect lower mortgage financing rates.

The foreclosure rate on apartment buildings or other types of multifamily properties is lower as compared to a single-family unit. This explains why mortgage lenders can offer competitive rates for investors of this type of property. This reduces operating costs which will bring more revenue in the long run.

If you are thinking of investing in property as a source of alternative income,

why not contact us today to discuss your requirements in more detail?

Phone: +353 86 325 0048 I Email:info@spirecapital.ie

Author: Deirbhile Finn-Healy

Prices from: €495,000 Rental yields: 6% – 8%

Spencer Dock is an exciting development of 1, 2 and 3 bedroom apartments, penthouses and offices setting new standards in urban living and working. Designed by the famous Architects Scott Tallon Walker, it is hailed as the new city quarter

0

0